")

Expanding the Debt Payment Plan?

You know me, always starting up a new idea before I finish the last one. It’s not a very good practice, but I’m on a roll.

You know me, always starting up a new idea before I finish the last one. It’s not a very good practice, but I’m on a roll.

Things are going so well with the debt payment plan that I have in place now (even though I’m only entering my second month…), I’m already looking to expand. Crazy.

But is it crazy?

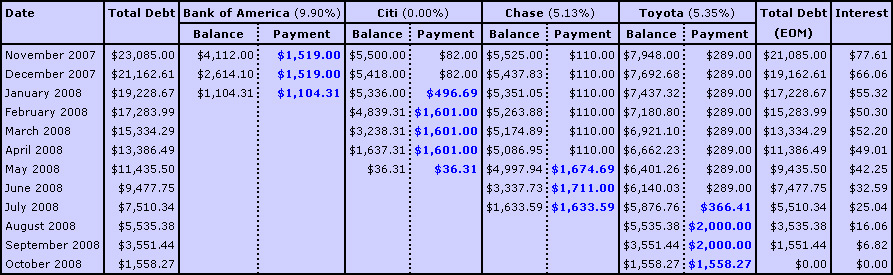

By the debt repayment chart, my total debt (credit card and auto loan) is supposed to be $21,162.61 at the start of December.

With one more day left in November, my balance is $19,897.44.

That’s $1,265.17 ahead of schedule!

Perhaps I should have made my plan more aggressive right from the get-go. But now I’m thinking maybe I should work my mortgage to the plan and cover all of my debts.

Now, I know, some out there think that pre-paying your mortgage is a bad financial move, and that your return will be better if you just invest the difference instead. And on paper, that’s probably correct.

But to me, long term investing is kinda like throwing money into a pile that you can’t touch. That’s probably because 90% of my investments come in the form of a 401k, where I really can’t get at it. It’s almost like it’s not there. Just a number on a statement.

Accelerating the mortgage wouldn’t really hurt my finances much — hey, and extra $1200 towards priciple is a pretty big dent — and the way things stand right now, that $1200 isn’t in my bank account anyway.

My day-to-day and month-to-month finances don’t change at all in the short term.

But a few years down the road, my biggest bill — the mortgage — would be gone. And that will definitely alter my month-to-month finances in a huge way. A positive way.

I put together a little chart this morning to spec out the various scenarios:

Right now, with my $25/week, plus an addition $50 or so to make the mortgage check a nice round number, I fall somewhere between the $100 and $250 lines.

Right now, with my $25/week, plus an addition $50 or so to make the mortgage check a nice round number, I fall somewhere between the $100 and $250 lines.

While that’s good, the idea of finishing off the mortgage somewhere around 2024 doesn’t sound very appealing. That’s a long way off. I’ll be 48 years old then?! The thought of overpaying my mortgage for the next 17 years doesn’t really interest me.

But let’s say I jack up my $25/week up to $250/week (or around $1000/month). Then the mortgage will be paid off sometime in 2014 — just 6 years away.

Owning my house, free and clear, while still in my 30’s. That’s appealing.

VERY appealing.

")

{kind=link}