")

![]() Grant from the Corner Office Blog recently posed a question on my posting about picking up a nickel that someone had dropped — and that no one else had any interest in.

Grant from the Corner Office Blog recently posed a question on my posting about picking up a nickel that someone had dropped — and that no one else had any interest in.

What are your thoughts on removing the penny (and nickel for that matter) from our financial circulation? There are some that argue we don’t need tangible currency at all, and can rely on bank cards entirely.

Everytime this comes up, while it’s a move in the opposite direction, it makes me think back to me time in Canada. I was already living in the States when the $1 bill was phased out in favor of the $1 coin — the loonie. Thinking back, I think that was around 1987.

Later, while I was actually back living there in the mid-90’s, they phased out the $2 bill, as well, in favor of another coin.

At the time, the idea seemed kinda neat. The coin was cool looking — two-tone!

But quickly you realized how terrible it really was. Vending machines suddenly raised their prices for the new $1 dollar (or even $2 dollar) coins. This, of course, was before you could slide paper money into vending machines.

But the biggest downside was that you ended up with heavy pockets. Let’s say you went out and broke a $20 on some pizza or something. More often than not, you’d end up with nearly $8 in change. That’s not chump change. After a week’s time, you’d be broke. But sitting on top of your dresser was $40 worth of coins.

Prior to the coins, loose change was always less than a dollar. By the mid-90’s, it was big money — but you still treated it like spare change. It added up quick — or more accurately, disappeared to the top of the dresser quickly.

A slight tangent — around the same time, a new banking feature was being test marketed on our campus by a company called Interac. The idea was just what Grant mentioned, you’d have an Interac card attached to your bank account that you could run through the Interac machines recently installed at all of the local establishments to make purchases. No need to carry any cash at all. Really, it was just a debit card. Before debit cards existed.

That experiment was obviously successful, though I never took part, with all of the debit card machines in every grocery store, and even fast food restuarants, these days. Back then, it was weird, and cutting edge.

But back to cutting out the penny, and maybe even the nickel, entirely. I happen to like the idea. It would definitely save the government a mint. But it would also likely cost the consumer more money too. Retailers, which would still accept cash, would need to “fix” their pricing so as to come out in 10 cent increments — and I can’t imagine many establishments would choose to round the number down. State sales tax would make it even a little trickier.

Another challenge is that while the actual physical currency would be eliminated, the value on paper would still exist — but there would be no way to, well, grasp it.

Being that we’re the type to bend over to pick up such small sums, I’d hate to see it considered as negligible.

I guess it’s an all-or-nothing type of situation. To me, you can’t eliminate the smallest value currencies unless you’re prepared to eliminate them all and fly with the bank card idea.

Of course, I’m totally in favor of that now.

(What I was thinking turning up my nose at it in 1994, I’ll never know…)

You know me, always starting up a new idea before I finish the last one. It’s not a very good practice, but I’m on a roll.

You know me, always starting up a new idea before I finish the last one. It’s not a very good practice, but I’m on a roll. Right now, with my

Right now, with my

This Thanksgiving, my wife and I attended the big football game between the two local high schools. The game itself was uneventful.

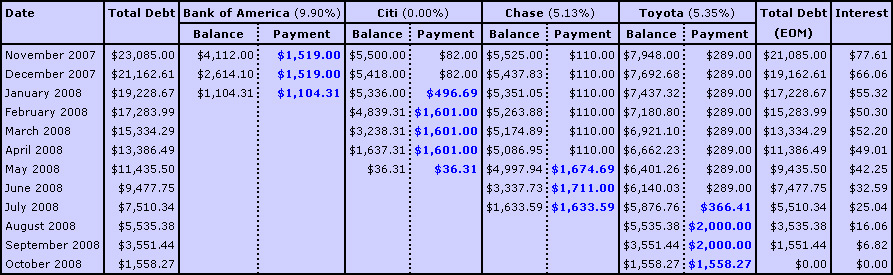

This Thanksgiving, my wife and I attended the big football game between the two local high schools. The game itself was uneventful. With my paycheck coming in today, a day early, because of the holiday, I just fired off another $800 towards my Bank of America credit card allowing me to cross November off on my

With my paycheck coming in today, a day early, because of the holiday, I just fired off another $800 towards my Bank of America credit card allowing me to cross November off on my  With all of the persistent news lately about how it will be harder and harder to borrow money, I’ve been really content with the fact that I’m well on my way to being out of debt and never really “borrowing” again.

With all of the persistent news lately about how it will be harder and harder to borrow money, I’ve been really content with the fact that I’m well on my way to being out of debt and never really “borrowing” again. Over the years, my wife and I have often received gift cards to area restaurants. Most of them are for borderline fancy places too.

Over the years, my wife and I have often received gift cards to area restaurants. Most of them are for borderline fancy places too. So this afternoon I put the finishing touches on my very first resignation letter which, barring any unforeseen circumstances, I intend to drop into the mail on Friday.

So this afternoon I put the finishing touches on my very first resignation letter which, barring any unforeseen circumstances, I intend to drop into the mail on Friday.

")

{kind=link}